Do you have a large sum of money in your account? Will it be enough to last through your retirement? In today’s economy, that’s not always guaranteed. However, with careful planning, you can still make your savings work for you.

If you have managed to save a lump sum, consider yourself at level 50 and now it’s time to work your way to level 100 by investing that money wisely. By using Systematic Withdrawal Plans (SWPs), you can manage your savings effectively while generating a stable monthly income during retirement.

In this article, we will explore strategies for using Systematic Withdrawal Plans and how they can help make your retirement funds last longer.

What is SWP?

SWP stands for Systematic Withdrawal Plan. It works like this: you invest a large sum of money in a mutual fund, and you are allowed to withdraw money regularly. You can schedule exactly how much to withdraw and when. For example, if you invest a lump sum of ₹1 lakh and withdraw ₹10,000 every month, the remaining money continues to stay invested and grows over time. This way not only will you stay invested but also have extra spending money. SWP turns your retirement savings or a lump sum into a steady monthly income, just like a salary, while keeping the rest of your money invested so it can continue to grow.

This way, you don’t have to rely only on bank interest or risk running out of money too soon at a vulnerable time.

How SWP Works: A Simple Example

Imagine you have saved ₹50,00,000 for your retirement. Instead of taking all the money at once, you put it in a mutual fund and start a SWP of ₹50,000 every month.

- Every month, you get ₹50,000 to pay for your needs.

- The rest of your ₹50 lakh stays invested and earns more money in the mutual fund.

- This way, your savings last longer and can even grow over time.

Think of it like marigold flowers that bloom all season. As long as you don’t pluck all the flowers at once, you keep enjoying the blooms. In the same way, SWP lets your money keep “blooming” even as you take some out every month.

What is the Difference Between SIP and SWP?

Think of SWP like a marigold that blooms throughout the season — as long as you stay invested, it provides a steady income. SIP, on the other hand, is like a lotus — it takes years to mature but eventually gives splendid results. Both are important and depend on what you want out of your hard-earned money.

Why SWP is Perfect for Retirement

SWP is very good for people who have retired and want money coming in every month. Here is why SWP is so helpful:

- Regular Money: Every month, you get some money. You can use it for food, bills, medicines, and other things. You know how much money will come, so it feels safe. The planning and execution are in your hands, and mutual fund advisors can help you execute it perfectly.

- You Can Change It: You can decide how much money to take out and how often. It’s flexible based on your needs.

- Money Grows: The money left in your SWP fund keeps growing, helping you beat inflation.

- No Worries: Your savings keep working and making more money even after you start taking monthly withdrawals.

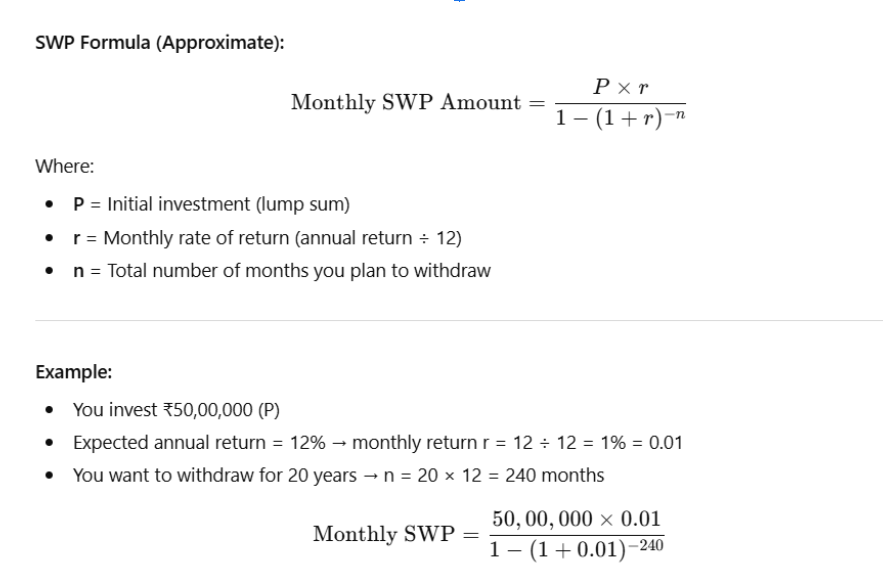

How to Calculate SWP?

First, understand the formula along with an example below.

SWP Formula (Approximate):

Monthly SWP Amount = (P × r) / [1 – (1 + r)−n]

Where:

- P = Initial investment (lump sum)

- r = Monthly rate of return (annual return ÷ 12)

- n = Total number of months you plan to withdraw

Example:

- Initial investment (P) = ₹50,00,000

- Expected annual return = 12% → monthly return r = 12 ÷ 12 = 1% = 0.01

- Withdrawal period = 20 years → n = 20 × 12 = 240 months

Monthly SWP = (50,00,000 × 0.01) / [1 – (1 + 0.01)^(-240)]

Alternatively, you can also use the formula below:

Tips for a Successful SWP

To make the most of SWP, as mutual fund advisors in Vijayawada, we ask you to follow these guidelines:

- Start with a realistic withdrawal amount: Too high, and your savings may dry up quickly; too low, and it may not meet your needs.

- Pick the right mutual fund: Balance growth and safety; avoid very risky funds after retirement.

- Review regularly: Adjust your withdrawals annually based on market shifts or major life changes.

- Plan for emergencies: Keep a separate emergency fund for unexpected costs.

- Reinvest any surplus: If you don’t use the full withdrawal, reinvest the leftover money in low-risk options.

- Set your SWP based on your budget: List your monthly expenses before deciding how much to withdraw.

- Avoid frequent adjustments: Changing your SWP too often can affect compounding; review only once or twice a year.

Benefits of SWP

- Provides a steady income during retirement.

- Lets your money continue to grow, protecting against inflation.

- Offers flexibility to withdraw as per your needs.

- Reduces stress about money running out too early.

Common Questions About SWP

- Can my money run out? Yes, if you withdraw too much too soon or if markets perform poorly. That’s why planning your withdrawals is important.

- Do I have to pay taxes on SWP? Yes, depending on the mutual fund type and your income level. Consult a tax advisor for details.

- Can I stop SWP anytime? Yes, you can stop or change the withdrawal amount anytime for full control.

Conclusion

Retirement should be a time to relax, enjoy hobbies, travel, and spend time with family—not worry about money. SWP is a smart way to turn your retirement savings into a monthly income, giving you financial security and peace of mind.

Think of SWP as a salary you get not from your boss but from your investments. It’s a flexible and simple way to make your savings last longer while continuing to grow. With careful planning and guidance from mutual fund experts, you can enjoy a comfortable retirement without fear of running out of money.